Capturing the Entire Real Estate Value Chain: REITs, REOCs, and Their Comparative Analysis

Understanding REITs and REOCs as standalone vehicles in a comparative analysis and evaluating their distinct roles in helping real estate sponsors capture the real estate value chain - end to end.

- Author

- Danish Jahangir Mir

While both REITs and Real Estate Operating Companies (REOCs) are capital markets vehicles for real estate investment and management, each has distinct characteristics and structures with certain commonalities. They can operate as standalone investment vehicles, or one can fulfill the shortcomings of the other by collectively operating as standalone vehicles as part of larger real estate ecosystem.

Table of contents

What is a REIT?

A REIT is a company that owns, operates, or finances income-generating real estate. Modeled after mutual funds, REITs offer investors, of all types, the opportunity to own fractional interests in real estate, earn dividends, and hold their investments in through liquid markets for long term appreciation.

An estimated 150 million Americans have made investments in REITs through a range of financial instruments including 401(k) accounts, IRAs, pension plans, REIT ETFs, and other investment funds. [source]

While typical real estate firms concentrate on selling properties once they are developed, a Real Estate Investment Trust differentiates itself by primarily acquiring real estate assets to be operated and managed as long-term investments within their portfolios.

Today, U.S. REITs own nearly $4.5 trillion of gross real estate with public REITs owning $3 trillion in assets. U.S. listed REITs have an equity market capitalization of more than $1.3 trillion. In 2021, REITs paid an estimated $92.3 billion in dividends to shareholders. [source]

REITs, by design, avoid corporate income tax. But to do so, REITs have to navigate a labyrinth of strict eligibility requirements such as distribution of at least 90% of its taxable income in the form of shareholder dividends, and deriving at least 75% of their gross income from rents from real property. If you want, you can learn about REIT fundamentals here, and come back to this article.

What is a REOC?

Real Estate Operating Company (REOC) is structured and taxed as corporations that predominantly own, develop and manage properties. Their income streams come from various avenues including, but not limited to, leasing commercial spaces, selling developed properties, and offering property management services. Some REOCs might also engage in ancillary businesses related to their properties, such as parking facilities or service-based amenities.

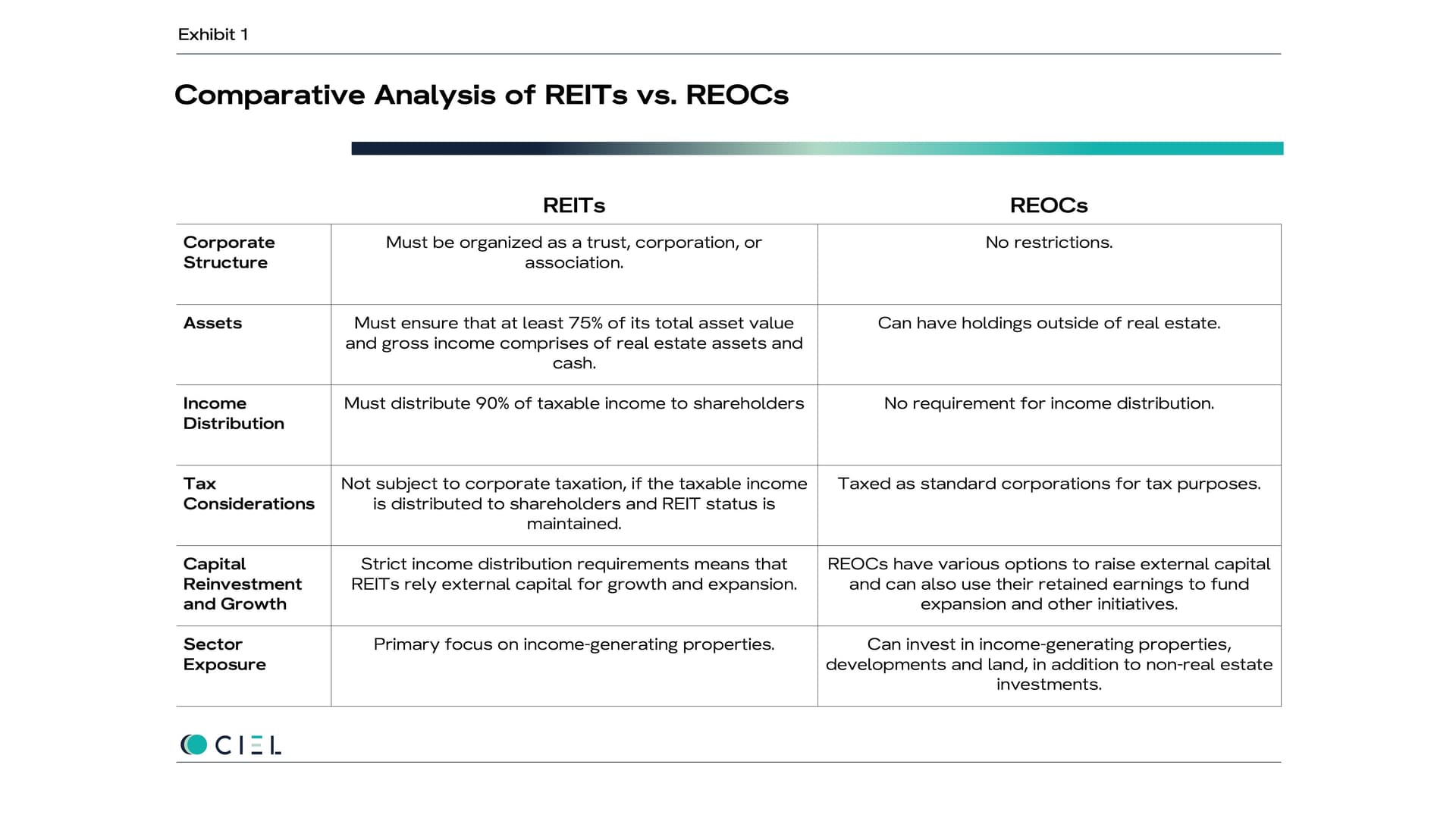

Differences between a REIT and REOC

The decision to go with a REIT or a REOC structure depends on a company's objectives, its growth strategy, the sector in which it operates, and the income expectations of its investors. For an investor, the decision depends on their income needs, risk tolerance, and investment horizon. The table below is a primer on the salient differences between the two vehicles. Choosing one or both requires a company's or investor's thorough analysis and understanding of the subtleties to make a well-informed decision.

Joint REOC-REIT Strategy

Some organizations might choose to have both a Real Estate Investment Trust and a Real Estate Operating Company operating under the same corporate umbrella. This strategy allows them to maximize the benefits of both structures: create a synergistic relationship that can drive growth and shareholder value.

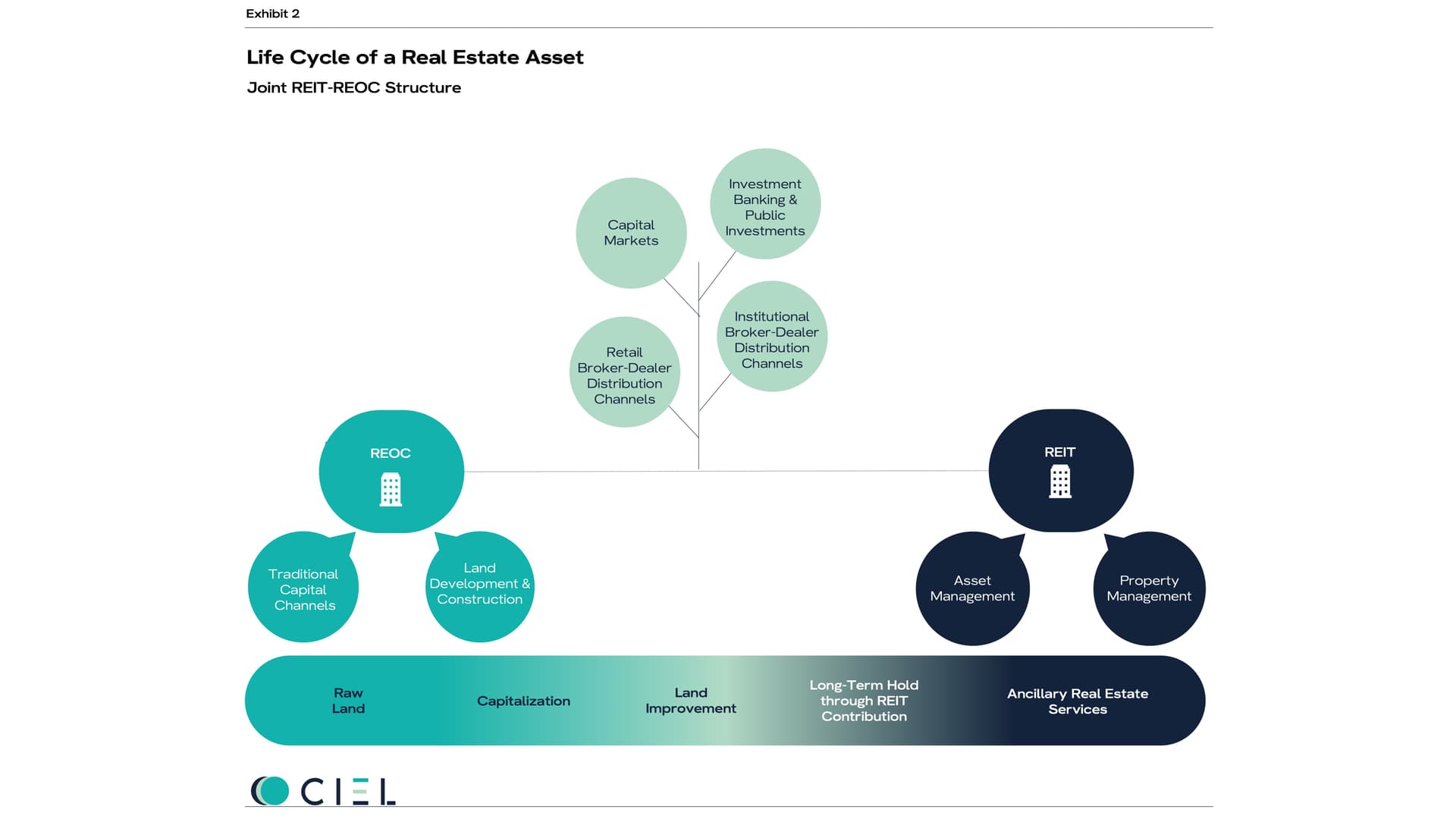

In this model, the REOC typically acts as the development arm, utilizing its freedom to retain and reinvest earnings to undertake real estate development projects and other growth-oriented activities. Once these projects are stabilized (i.e. they are income-producing), they can be transferred to the REIT via a 721 exchange UPREIT (or downREIT) transaction, where they become part of a portfolio of income-producing assets that provide regular dividends to shareholders of the overall platform.

Lifecycle of a Property Under this Strategy

The infographic below is a depiction of the various functions that go into capturing the entire real estate value chain of a real estate asset, and how this can be created into a repeatable process as part of a larger ecosystem.

Strategic Advantages of a Joint REOC-REIT Structure

A joint REOC-REIT structure allows companies to balance growth and income objectives while maintaining the tax advantages of the REIT structure. The joint structure enable real estate firms to capture the entire real estate value chain (from land to stabilized properties), stay vested in real estate projects for long-term tax-deferred gains, tap into the capital markets to access capital for all real estate-related activities (land acquisition, development, construction, operations and management), and unlock fractional or partial liquidity for its shareholders through the stock markets.

From a tax perspective, the REIT provides a tax-efficient vehicle for distributing income to shareholders, while the REOC to REIT asset transfers allow for tax-deferred growth.

A limited partnership can be built into a REOC structure to acquire land under the 721 exchange regime.

From a growth perspective, the REOC can use its retained earnings to fund new acquisitions or developments, while the REIT can focus on managing its portfolio of income-producing properties and providing steady dividends to shareholders.

Additionally, multiple REITs can be added to this structure, each with a sector-specific focus, which would allow the REOC to invest in and develop opportunities in multiple sectors. For example, the REOC could develop a master-planned community with multiple land uses (such as retail, residential, healthcare, senior living, and hospitality) and each of these parts of the development could be separately contributed to in-house REITs specializing in each of those sectors, or to Baby REITs with one parent REIT.

Why not just sell the projects for cash and reinvest?

That is because a real estate company with a joint REIT-REOC structure can access the capital markets to raise the capital it needs for investments, which allows it to remain vested in proprietary assets. This dual structure is a means to create a pipeline of stable, income-producing properties for the REIT through the REOC. This allows the REOC to singularly focus on unlocking real estate equity and building a long-term stream of income through the REIT for reinvestment into growth opportunities.

In addition to development, REOC structures are also used for other real estate functions: sales, leasing, and property management. A REOC can build these functionalities to provide services to in-house REITs to create additional streams of income; this is especially lucrative when in-house REITs are opened up to the contribution of assets by real estate owners outside the company's wheelhouse.

Real Estate, REITs, REOCs, and M&A

M&A strategies in real estate vary depending on the stage of a real estate company’s lifecycle. One-off property acquisitions are generally financed through traditional sources such as senior mortgages, preferred equity, and mezzanine financing. Portfolio acquisitions are also not uncommon, especially by real estate companies (including REITs and REOCs) that have excess balance sheet cash or access to structured financing options such as corporate bonds. In some cases, small or midsize real estate firms have merged to form one large real estate holding or operating company, which in some cases, have converted into REITs or REOCs down the road.

Broadly, M&A in the public markets that is through public vehicles such as REITs and REOCs is not all that different except with respect to three main factors: type of M&A capital, type of investor audience, and access to publicly traded stock. Public real estate vehicles have access to a plethora of M&A financing options, even more, if they are publicly traded - various types of securities offerings, including those exempt from registration requirements, corporate bonds, and crowdfunding, to name a few. We have provided a comprehensive overview of these capital channels in our article here.

Generally, going public as a real estate company requires a sizeable portfolio with substantial equity. And it is generally such companies that choose to opt for the go-public route, including REITs and REOCs. Alternatively, multiple private companies may merge their portfolios under one real estate company and take the NewCo public.

Going public allows owners to (i) unlock equity in their assets or companies to fund expansion goals, (ii) raise institutional and retail capital through multiple channels for M&A objectives, (iii) exhibit stellar historical performance to raise capital and build a captive investor audience to continue raising capital for M&A with certainty, and (iv) use the public vehicle (REIT, REOC, or real estate holding company are common structures) to fund M&A transactions with stock or OP Units (sometimes partially, sometimes with a combination of cash).

M&A strategies become important for real estate companies when they want to achieve scale, diversify into new geographies and sectors, use tax-advantageous structures to maximize the profitability of existing assets or portfolios, or combine resources, market presence, and negotiating power by merging with other players in the market.

For example, a real estate company looking to roll capital gains in an asset into a new investment, including new assets in a different sector, may enter a 1031 exchange transaction. Alternatively, a real estate company looking to roll capital gains in a portfolio into a transaction that defers capital gain taxes, and opens up the option for liquidity and long term appreciation, may explore an UPREIT transaction to avail 721 exchange, and take back OP Units that they may convert into common stock of the partner REIT to free up liquidity in tranches (not all of it at once).

Notable examples of M&A include (i) Ventas, a healthcare REIT that expanded into the life sciences sector through the acquisition of Wexford Science & Technology in 2016, and (ii) Prologis's acquisition of Industrial Property Trust, in 2019, to diversify its presence in several high-growth markets.

Mergers and Acquisitions can play a pivotal role in a REIT's growth strategy - help achieve scale, enter new markets, diversify asset portfolios, and realize operational efficiencies - but only if they are meticulously planned and seamlessly executed.

M&A strategies for a real estate ecosystem such as the one we have discussed above, are generally more nuanced and require a thorough analysis of the financial, legal, and tax implications of M&A activities, especially to identify the highest-return yielding targets. A diverse ecosystem, with various structures that have distinct financial, legal, and tax benefits, provides an incredible amount of optionality - tax deference, liquidity, capital access, and multiple streams of income. To learn more please feel free to schedule a free consultation with our real estate M&A team here.

How CIEL Can Help

CIEL has been on both sides of the table, real estate owner/developer and REIT/REOC sponsors and managers, we understand and appreciate the nuances.

Our team uses empirical analysis to help real estate sponsors optimize their growth and expansion strategies, identify the next frontier for their real estate operations, and build ecosystems around their core capabilities to maximize value from their real estate investments.